What if the greatest trick the market ever pulled was convincing investors that we’re still in a bear market?

The S&P 500 declined 23 percent between January 3 and June 16. It is up 14 percent since then. The tech-heavy Nasdaq, which dropped 32 percent, has since gained 20 percent. And yet worried fund managers are holding the highest level of cash since after the September 11 attacks in 2001, according to a Bank of America survey, and they are even less willing to take risks than after Lehman Brothers collapsed in 2008.

The mid-June low is notable. On June 14, the US Treasury 10-year bond yield reached a high of 3.49 percent. Two days later, the 30-year mortgage rate peaked at 6.7 percent. And the average price across the country of a gallon of gas surpassed $5 for the first time. The annual headline inflation rate increased from 8.3 percent in April to 8.6 percent in May and 9.1 percent in June, its highest level since November 1981. July’s 8.5 percent rate represents a downshift.

On June 15, the Fed raised the federal funds rate by three-quarters of a percentage point in its most aggressive hike since 1994. Futures markets showed investors expecting the fed funds rate to hit 3.6 percent by the end of the year, above the Fed’s forecast of 3.4 percent. This past December Fed committee members predicted a 0.9 percent end for 2022.

In the same week came a record high in the number of economics stories using the word “recession” in either the headline or the first paragraph: 21,576. Meanwhile, the small business (NFIB) outlook hit an all-time low. And the AAII bull–bear sentiment ratio came in lower than at the height of the pandemic. Asking if we were “Feeling unwell?”, Bloomberg BusinessWeek put a vomit bag on the cover of its magazine imprinted with the words “For market upheaval, economic turbulence and other discomforts.”

Source: The New York Times, Wall Street Journal, MoneyWeek, Bloomberg Businessweek, The Economist

The most speculative pockets of the market, including Cathie Wood’s Ark Innovation Fund (ARKK) and biotech, bottomed on May 12. That was the first sign. Then the Nasdaq started outperforming from May 23, despite a 75-basis-point jump in 10-year yields. Additionally, just 10 percent of the companies in the S&P 500 were trading above their 200-day moving average on June 13. A year ago, the proportion was more than 90 percent.

Likewise, we observed encouraging developments in China. On May 26, the State Council convened an unprecedented videoconference with more than one hundred thousand officials across the country. Premier Li expressed concern about the possibility of the Chinese economy “slipping out of the reasonable range.”

Nearly 2 trillion yuan ($296 billion) in special purpose bonds have since been issued, alongside 1.1 trillion yuan ($163 billion) in additional stimulus funding through the policy banks. Despite earlier restrictions, China also issued a record 1.5 trillion yuan ($225 billion) in local government bonds in June. According to analysis by Trivium China, this might provide substantial economic support of around 2.5 percent of GDP.

It remains to be seen how much of the infrastructure-centered stimulus is used properly. We reckon this is the “socialism put” in action, however, ahead of the twentieth National Congress of the Chinese Communist Party in the fall. Several onshore managers put it more bluntly: “with Beijing bombing investors with positive headlines, it is simply difficult not to be bullish.”

The Shanghai Composite index has trended up since April 26. China’s tech stocks bottomed in March and are since up 50 percent. This is despite covid-related restrictions, an imploding property sector, and lingering regulatory uncertainty in the tech space. Chinese stocks are climbing a great wall of worry.

Source: Reuters

We’ve been on the lookout for a third bull phase. Here’s a reminder of the prior phases.

The first phase (March to September 2020) was a policy-induced rally. With unprecedented fiscal and monetary action combined, the global stimulus tally exceeded $20 trillion. The S&P 500’s forward 12-month price-to-earnings (PE) multiple jumped from 13 at the March lows to over 23, or 76 percent, offsetting a 12 percent drop in earnings for the 2020 calendar year. The S&P 500 soared 64 percent to reach its September high before falling 11 percent.

The second phase (September 2020 to December 2021) was a low-conviction rally. Labor shortages and supply chain bottlenecks were becoming more of a problem as the virus continued to spread. Many were surprised by the strength of corporate earnings, which surged by 54 percent and compensated for the multiple compression. The S&P 500 gained 50 percent.

The third phase has a well-worn path: first, non-US markets tend to outperform after lagging in the first two. Despite the war in Ukraine, France’s CAC index and Germany’s DAX index are up 13 percent and 10 percent, respectively, since March. The S&P 500 is flat over the same period, and it has lagged the iShares MSCI ACWI ex US ETF (ACWX) by 4 percent.

Second, cyclical sectors like technology and consumer discretionary considerably outperform. The former has outpaced the S&P 500 by 8 percent since mid-June, while the latter has done 16 percent better. Growth stocks are also retaking the lead, beating value by 20 percent thus far. This is consistent with the third phase.

Third, government bonds significantly underperform stocks and high-yield bonds. Since March, the stock-to-bond ratio (SPY/TLT) is up 13 percent, while high-yield bonds (HYG) have outperformed by 10 percent. Corporate and high-yield bond spreads can tighten during this phase and deliver positive returns, despite falling creditworthiness and rising defaults.

Fourth, we cautioned that zero-yielding commodities face a headwind from an increase in real interest rates. Prices for oil and base metals have dropped by more than 30 percent from the highs during the Russian invasion. Lumber, soybeans, cotton, and wheat all finished the second quarter at or below their March levels. The Bloomberg Commodity Index fell 20 percent from its June peak.

Fifth, EM carry trades make a comeback as risk appetite increases. Even while the dollar index rose to 52-week highs against the euro, the British pound and the Japanese yen, it has remained relatively stable since March versus a group of EM currencies. The dollar typically weakens during the third phase.

While we’re awaiting more signs that the eleven-year dollar bull market is coming to an end, there’s enough evidence to suggest that the third bull phase for stocks is upon us. We think the S&P 500’s closing low at 3,666 on June 16 may have been the bottom.

Source: CNBC

At Stray Reflections’ Palo Alto dinner, the guests submitted that a bullish market would require China loosening, inflation rolling over, and stocks not going down on earnings misses. We’re seeing all three now.

According to FactSet, companies that reported second-quarter results below analysts’ estimates witnessed an increase in their stock price, namely, an average gain of 1.2 percent from two days prior to the earnings announcements to two days thereafter. This contrasts with the five-year average stock price decline of 2.4 percent during the same span.

On June 16, the S&P 500’s forward PE ratio fell to 15.5, below both the 5-year and 10-year averages of 18.6 and 16.9. Since then, it has increased by 15 percent to 17.8. We see room for multiples to expand further. Small-cap stocks in the US are trading near their lowest valuations ever.

The first stage of valuation correction coincided with the sharp rise in bond yields. The 10-year yield jumped 100 basis points in just three months. The next climb in yields will be much slower as year-over-year inflation readings are cooling off. This won’t harm multiples. Despite all the doom and gloom, we believe that a recession is not on the horizon, which will cause the next step of the valuation correction.

The Business Cycle Dating Committee of the National Bureau of Economic Research determines when expansions start and end, defining recession as a “significant decline in economic activity that is spread across the economy and lasts more than a few months.” A negative GDP growth rate for two consecutive quarters has no significance.

The 2001 recession only saw one quarterly GDP contraction, and despite GDP contracting for two consecutive quarters in the mid-to-late-1940s, there was no recession. A historic drop in consumer confidence and bearishness shows up in the survey data, but consumer spending has held up so far this year. The electronics and appliances category is the only one that’s seen a decline in spending from 2021.

The Bureau of Labor Statistics has a metric called the index of aggregate weekly payrolls, which is the product of jobs, wages, and hours worked. It’s a rough proxy for the spending capacity of the workforce, and it increased by 0.6 percent month-over-month in June to a record high of 172.4, reflecting a 9.4 percent jump from a year ago. Before the pandemic, the annual growth rate of the payrolls metric was trending at around 5 percent.

Apart from a few announcements at prominent tech companies, layoffs are near record-low levels. In June, the layoff rate was just 0.9 percent, marking the sixteenth straight month that it was below the 1.1 percent pre-pandemic low. Initial claims for unemployment insurance, while above a six-decade low of 166,000 in March, remain depressed at levels associated with economic expansion.

Employers may be reluctant to shed workers amid persistent labor shortages. With nearly two job openings per unemployed person, this is a very tight labor market. Some employers took to earnings calls to express hesitation around reducing headcount, even as demand slows.

Source: Getty Images

Higher rates will have an impact, but it should all be seen in the context of a robust economy that is simply returning to a more normalized level of activity after growing 5.7 percent in 2021—the fastest pace since 1984.

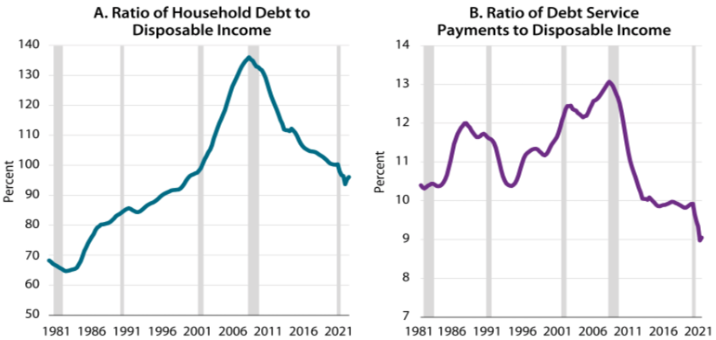

The US economy is far more resilient to higher interest rates than bears like to believe. Despite an overall increase in consumer borrowing, the boost to incomes and the fall in interest rates have resulted in unprecedented declines in the household debt-to-income ratio, which is at its lowest level since the mid-1990s. And the cost of servicing debt relative to income is at its lowest point since at least 1980 when the data series began.

Home mortgages, the largest component of household debt, have increased by more than $1.1 trillion since 2020. But mortgage debt is now about 65 percent of personal disposable income, compared to around 100 percent at the end of 2007.

People with higher incomes and credit scores have accounted for much of the growth in mortgage borrowing. Since early 2020, borrowers with super-prime scores (above 760) have made up 70 percent of those taking out mortgages, while subprime originations were just 2 percent of the total. In contrast, super-prime borrowers made up 25 percent of originations in the mid-2000s while subprime borrowers made up 13 percent.

Pertinently, the share of households with adjustable-rate mortgages (ARMs) is miniscule at less than 10 percent of the mortgage market, and the inventory of homes for sale remains low. Recall that in February 1994, 22 percent of buyers chose ARMs; by the fall, it was 42 percent as the Fed hiked aggressively. Home prices continued to rise throughout the surge in rates. We can see the same thing happen again. The slowdown in the housing market is temporary. We’re bullish on homebuilding stocks.

In aggregate, relatively low debt ratios should limit the impact of higher interest rates on the housing market and overall consumer spending. We think that the strong financial position of households will fuel the economic expansion in the upcoming months and years.

Source: Brookings

Our optimistic assessment contrasts with the US Conference Board’s Measure of CEO confidence, which has fallen close to the 40 level, often a signal of declining profits or a negative change in earnings year-over-year.

The macro picture is distorted. The deflated base prices of March 2020 played a significant role in explaining why inflation didn’t start to seem alarmingly high until March 2021. Core inflation reached its high in March this year as a result of base effects normalizing. Now the inflation picture is reversing.

The pandemic-deflated base prices also resulted in the S&P 500 reporting year-over-year earnings growth of 91 percent and 88 percent in the first and second quarters of 2021, respectively. Bank profits nearly doubled due to the release of reserves that had been placed aside for loan defaults during the pandemic that never materialized. Banks reduced loan-loss provisions by $14.5 billion and $7.6 billion in the first and second quarters of 2021.

This explains the decline in bank profits this year. It’s mainly down to the release of loan-loss reserves in 2021 overstating profits. Lending is actually up at nearly all the banks. Consumers and companies increased their borrowing from the largest banks by an average of 6 percent in the second quarter compared with the same period last year.

The biggest gains were in corporate loans, which rose nearly 20 percent from a year earlier at both JPMorgan and Bank of America. JPMorgan raised its estimate for net interest income for the year to $58 billion, a $2 billion increase from its forecast of only two months ago. This is not what happens in an earnings recession.

The energy sector is the largest contributor to the S&P 500’s earnings growth in 2022. Without energy companies the index would report an earnings decline of 4.1 percent in the second quarter, instead of a 4.3 percent increase. But if the financials sector were excluded, then earnings growth that quarter would improve to 10.1 percent.

Consider another anomaly. On its investment in Rivian Automotive, Amazon booked a $7.6 billion pre-tax valuation loss in the first quarter. The consumer discretionary sector would have recorded earnings growth of 3.8 percent rather than a 32.6 percent decline if Amazon had not been included. The implication is that the earnings picture is more nuanced and not as awful as many assume.

Source: Conference Board

Despite the downward revisions, S&P 500 earnings are still expected to grow by 8 percent in 2022 (earnings per share coming in at $225) and a further 8 percent in 2023 ($244). Although there are risks to the downside, we think the earnings forecasts look achievable.

According to Factset, actual earnings reported by S&P 500 companies over the past five years have exceeded estimated earnings by an average of 8.9 percent. On a ten-year horizon, the positive earnings surprise was 6.5 percent.

As we move beyond the base effects that are suppressing earnings, and as economic activity picks up (most of the rebound owes to the passage of time), it will spur greater risk-taking in global markets. Nervous investors require validation that this is more than just a “suckers’ rally.”

Let us ask again. What if the greatest trick the market ever pulled was convincing investors that we’re still in a bear market?