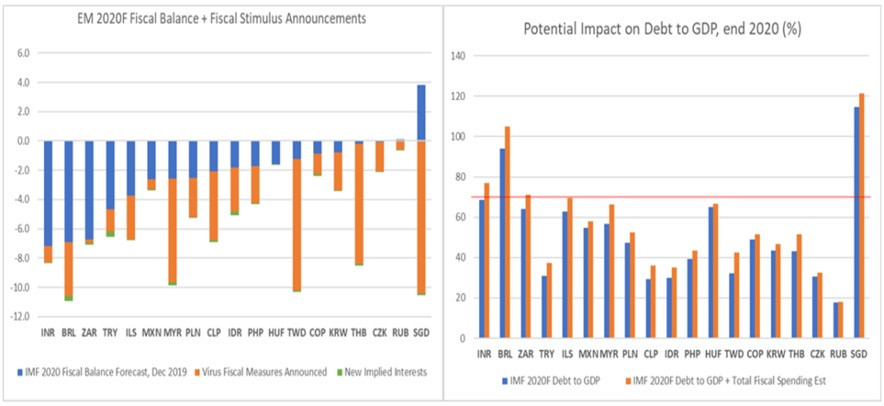

The left chart shows the IMF’s fiscal balances forecast for end-2020 in blue (from December 2019), to which the Speaker added up the headline fiscal packages announced by EM governments to tackle the virus and additional interest payments implied by the yield moves. He notes the vast majority of incremental fiscal spending is likely to be financed through new debt issuance (or indirect central bank monetization).

Source: IMF, Bloomberg

Putting those total deficits into context, which are conservative as this does not take into account the loss of revenues from the recession, the Speaker identifies a number of EM countries that look vulnerable: India, Indonesia, Brazil, Mexico, Hungry and South Africa. He thinks we are only “halfway through” the EM repricing.

What rescued emerging markets in 2008 was China’s massive stimulus, but this has remained absent through this crisis. A participant noted that fiscal stimulus is ineffective when the economy is half-shut. He said that factories in Wuhan are opening up and he expects a strong fiscal response by the end of this month. However, it would not match the scale announced in 2008 or 2016.

Many EM countries are left alone to confront multiple crises—a health crisis, a financial crisis, and a collapse in commodity prices, which interact in complex ways. Some will have to make the difficult choice of re-opening economies because social distancing is not practical to fight back the virus. This could lead to social unrest and an even bigger economic fallout down the road.

Photo: Unsplash